Beware of Financial Alchemy

On the folly of chasing yield, why the stock market isn't a puzzle, and how pattern recognition can backfire.

In 1822 a Scottish soldier sold £200,000 of bonds offering a 6% yield. The bonds were backed by the full faith and credit of Poyais, a territory in Central America. Unfortunately for investors, Poyais didn’t exist and they lost everything.

In 2020 people are still attracted to investments that aren’t what they seem. This post covers three red flags to avoid.

The Folly of Chasing Yield

Safe bond investments no longer offer a meaningful return. This has led to demand for “bond alternatives” with higher yields.

Income-oriented investors tend to buy first and ask questions later. History shows how stretching for yield can end:

There are two bond alternatives to be wary of:

Dividend Stocks: Swapping out a low yielding bond fund for dividend stocks misses the point of a bond allocation: safety. Dividend stocks aren’t immune to stock market volatility. For example, Vanguard’s high dividend fund (VYM) fell 32% in 2008.

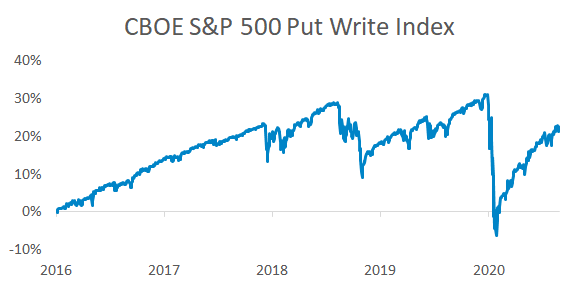

Selling Options: Like bonds, selling options generates income. Unlike bonds, the strategy crashes along with stocks. An S&P 500 option selling index erased four years of gains in a month:

Dividend stocks and selling options aren’t inherently bad, but swapping bond money into risky strategies is a recipe for disappointment.

I disagree with the narrative that older investors now have to take more risk. Today the 10-year Treasury yields 0.8%. It averaged 2.2% over the past decade. If this year’s drop in rates breaks someone’s financial plan then it was never sustainable to begin with.

Betting on Pattern Repetition

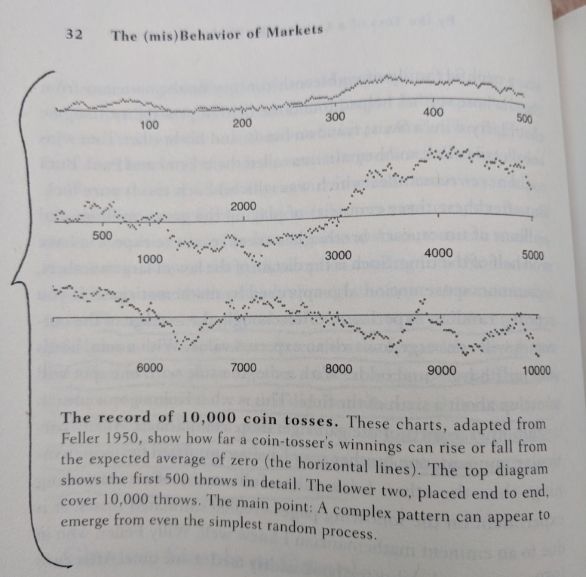

We have a tendency to see patterns everywhere and financial markets are no different. Complex patterns can emerge from random processes. 10,000 coin tosses look awfully like a stock chart:

Some investors base their portfolio around historical patterns repeating. This is optimizing for what has worked, not what will work.

Investing isn’t like betting on sports where the bet is independent of the game. Investors are on the field and their behavior controls the outcome. But just as players come and go and coaching styles evolve, market relationships can also change. Historical market patterns aren’t etched in stone and some may ultimately prove to be a fluke.

A pattern since 1980 is that Treasury bonds have protected portfolios from stock crashes. The yield on a 10-year Treasury would have to fall to -1.0% from current levels to match their return in 2008. Is it possible? Yes. Should investors continue to rely on Treasuries to hedge stocks? No.

Sacrifice and Success

Sacrifice is necessary for success in life and investing. Someone researching portfolio strategies but refusing to save more than 3% of their income is like spending hours at the gym and eating donuts for dinner. They might feel good about doing something but they won’t actually make progress until they make a sacrifice.

Investors have to embrace the fact that they cannot predict the best portfolio for the future. The silver lining is… that’s OK. Meb Faber showed that ten different strategies earned similar returns over four decades. Most importantly, high fees transformed the best performing portfolio into the worst. There are only a few things you can control that have a big impact on your finances:

- If you’re young, how much you save

- If you’re retired, how much you spend

- How you behave when markets panic

- Your allocation between stocks and bonds

- How much you pay in fees

Everything else is a rounding error. The issue is we tend to focus on the rounding errors. It’s easy to get addicted to an endless rabbit hole of new investing ideas. Announcing a new goal, not even achieving it, gives you a hit of dopamine. Investors get a similar psychological payoff when they constantly buy and sell, even if the activity doesn’t add value.

The truth about investing in 2020 is there isn’t an easy fix for high stock valuations and low bond yields. No strategy can magically transform today’s low return opportunity set into a high return future. So what can you do? Focus on what you can control and don’t get tempted by someone promising they can turn lead into gold.