How to Squeeze the Most Value Out of Credit Card Points

Have you ever wondered if you’re getting the most value out of your credit card points? This post explains how to make your points stretch further, avoid annual fees, and ranks the most valuable sign-up bonuses.

Have you ever wondered if you’re getting the most value out of your credit card points? This post explains how to make your points stretch further, avoid annual fees, and ranks the most valuable sign-up bonuses.

Travel blogs make money from affiliate links that pay them if you get approved for a card. This creates an incentive to push cards with high affiliate payouts and results in less coverage of other cards. This post doesn’t have any affiliate links.

Using points, I’ve traveled to the below places for substantially less than regular cash prices.

Why Points are Valuable

The most valuable use of credit card points is booking flights and hotels – not statement credits or free offers from credit card websites. Each point program has a different name: Chase has Ultimate Rewards, American Express has Membership Rewards, etc. There are two types of point programs:

Flexible points, such as Chase Ultimate Rewards, can be transferred to a variety of airline and hotel partners

Program points, such as World of Hyatt points, can be used mainly at Hyatt hotels

Flexible point programs tend to be more valuable because you can transfer them to multiple companies. Most of these transfers are one-to-one, meaning 100 Citi ThankYou points transfer to 100 JetBlue TrueBlue points.

The value of a flexible point program is a function of its transfer partners and conversion rates. For example, Chase Ultimate Rewards are generally regarded as more valuable than Citi ThankYou points since Chase has more frequently used transfer partners:

Chase Transfer Partners

Citi Transfer Partners

Point Redemption Example #1 – Air Travel

Loyalty programs have redemption charts that show how many points are required for a given booking. Here’s a portion of the American Airlines redemption chart for domestic travel in coach:

A one-way US flight over 500 miles with MileSAAver availability takes 12,500 points. MileSAAver is the most affordable type of redemption, which means it tends to get quickly booked up. Let’s assume you could book the MileSAAver tickets for both flight legs – this would mean you’d redeem 25,000 American Airlines miles for a round-trip ticket.

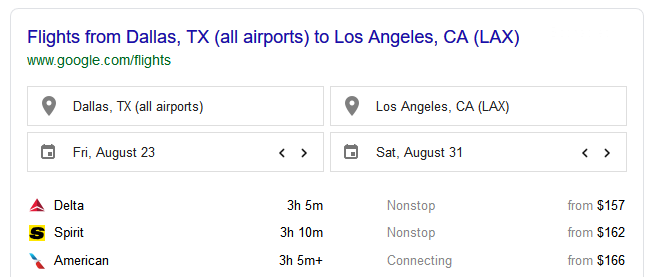

There are both good and bad redemptions. Using 25,000 American Airlines miles for a flight from Dallas to Los Angeles would be a bad redemption since the cash price is typically $150.

This means you’re using your points at a value of only 0.6 cent per point ($150 / 25,000 points). You’d be better off taking a statement credit at one cent per point.

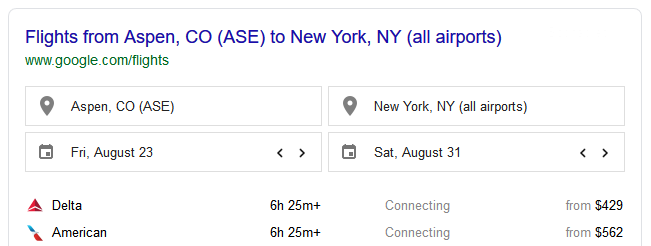

In contrast, a flight from Aspen to New York would require the same 25,000 points but typically costs $560 on American.

This would more than triple the redemption value to 2.2 cents per point ($560 / 25,000 points). You’re squeezing much more value out of the same number of points.

The highest redemption values are with business and first class tickets. For example, using 100,000 points for a ticket that’s typically $5000 translates to a value of 5 cents per point. This is how people make videos like:

I would personally prefer to get two or three economy tickets rather than one business class ticket, but it’s up to you. The main thing to remember is that you should try to use points for high-value redemptions.

Point Redemption Example #2 – Hotels

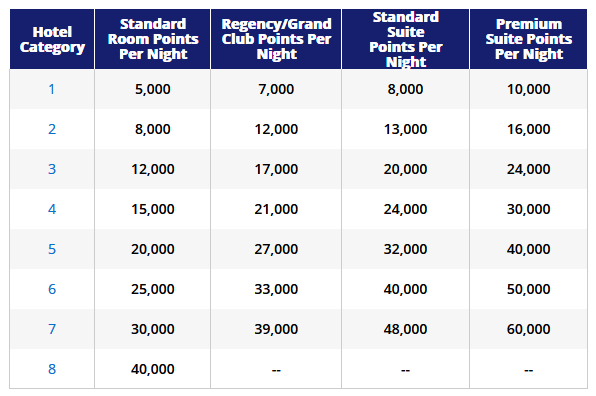

Here’s Hyatt’s redemption chart:

It takes 12,000 Hyatt points for a free standard room at a category 3 hotel. You can earn Hyatt points directly through the Chase Hyatt card or through a Chase card that earns Ultimate Rewards (since Hyatt is a transfer partner of Chase). You could also transfer airline points to Hyatt, but airline-to-hotel and hotel-to-airline transfers are poor redemption values.

Just like there are good and bad airline redemptions, the same principle applies to hotels. Here are three valuable Hyatt redemptions:

- The category 6 Park Hyatt Buenos Aires for 25,000 points. Typically $500, redemption value of 2 cents per point

- Any category 1 Hyatt House for 5,000 points. Typically $125, redemption value of 2.5 cents per point

- The category 7 Park Hyatt Paris for 30,000 points. Typically $750, redemption value of 2.5 cents per points

Alliance Programs – The Shortcut to Higher Redemption Values

For flexible point programs like Chase and American Express, it’s important to know that you’re not restricted to the immediate transfer partners. For example, you might have a bunch of American Express Membership Rewards and want to book an American Airlines flight. American Airlines is not an American Express transfer partner – but British Airways is. Both American Airlines and British Airways are Oneworld alliance members.

So you would transfer your American Express Membership Rewards to British Airways Avios, then use Avios (with their redemption chart) to book a flight on American Airlines.

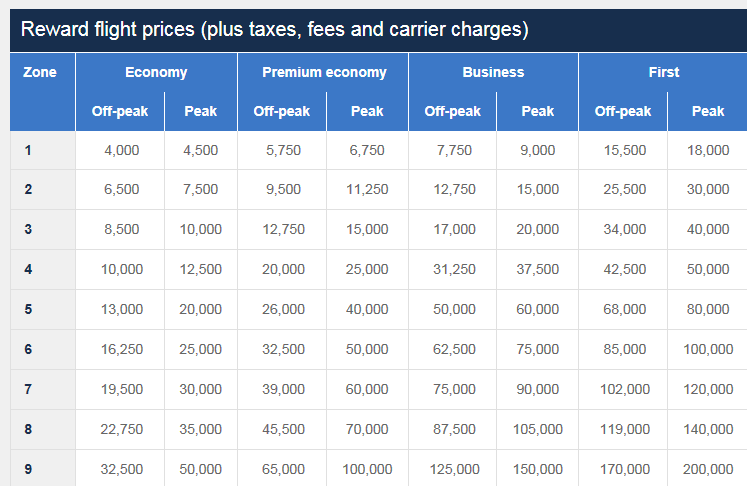

There can be a huge difference in redemption values between alliance members. Let’s say you wanted to fly from Atlanta to Austin. The previous American Airlines redemption chart shows it would take 25,000 miles to fly round trip at MileSAAver availability. Check out the British Airways Avios redemption chart:

Atlanta to Austin is a ~800 mile flight, so that qualifies as a zone 2 redemption. It would take 15,000 British Airways Avios for a peak-season round trip economy ticket. Chase Ultimate Rewards transfer one-to-one with Avios, so it would only take 15,000 Chase Ultimate Rewards for a free flight (far fewer than 25,000 American Airlines miles).

Redemption Sweet Spots

A points program can’t be uniformly labeled good or bad. Like in the British Airways example, each program has sweet-spot redemptions. Here are some good US flight redemptions for the two most popular flexible point programs:

- Chase Ultimate Rewards: Fly to Europe using Singapore Airlines KrisFlyer miles, Australia with Air France/KLM FlyingBlue miles, domestic US flights with Southwest Rapid Rewards miles

- American Express Membership Rewards: Fly to Japan using ANA Mileage Club miles, Hawaii with Air France/KLM FlyingBlue miles, a round-the-world ticket with ANA Mileage Club miles

The easiest way to find the best points redemption for a given destination is to Google “best way to fly to _________ with points.” Before using points, search to be sure you’re getting the highest redemption value.

Sign-up Bonuses: Where the Most Value is Found

Much is written about cards that earn 2-3% back on spending categories, but the reality is that people who get the most value out of credit card points do so by earning multiple sign-up bonuses.

For example, one of the higher point multiples on everyday spending (not subject to a cap) is 2x. Let’s say you spent $3,000 on a card every month. That’s 72,000 points per year. That’s a year of spending when you could have earned that amount of points in a single sign-up bonus.

Spending bonuses are a nice benefit but it’s not how to score a free Lufthansa first class ticket. There’s a reason why Reddit’s points community is called r/churning – a nickname for the process of applying for a card, capturing the sign-up bonus, closing or downgrading the card, and then re-applying.

Churning has become more difficult as card issuers have introduced application restrictions. Personally, instead of churning, I’ve just applied to a variety of different cards.

Calculating the Cash Value of a Card’s Sign-Up Bonus

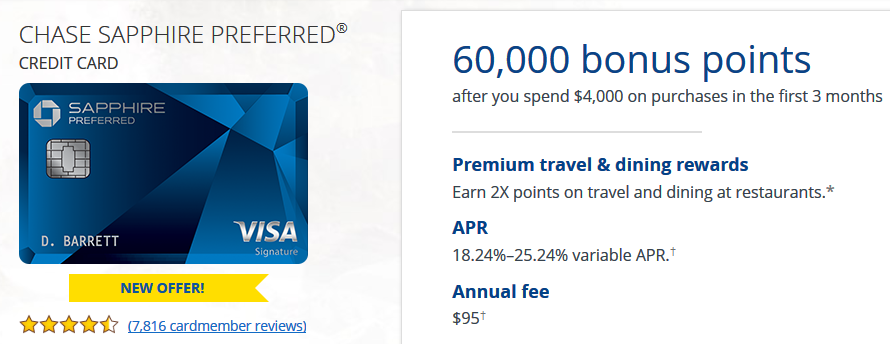

Let’s deconstruct an example sign-up bonus. One of the most popular cards is the Chase Sapphire Preferred. You can earn 60,000 Chase Ultimate Reward points if you spend $4,000 in three months.

On average, Chase Ultimate Rewards are valued at 2 cents per point. 60,000 x 0.02 = an approximate redemption value of $1,200. The card’s annual fee is $95 and is not waived the first year, so I deduct that from the value of the sign-up bonus. You can realistically expect to book $1,105 of free travel with this sign-up bonus.

The actual value you get depends on your redemptions. Bad redemptions (1 cent per point or lower) mean your points won’t stretch as far, but you could easily squeeze more than $1,500 out of the bonus if your average redemption value was greater than 2.7 cents per point.

Some cards provide extra benefits beyond a sign-up bonus and spending multiples. One example is the American Express Platinum, which gives you $200 in annual airline fee credits, $200 in annual Uber credits, $100 in Global Entry or TSA Pre-Check credits, and access to Centurion airport lounges. The value of these benefits depends on if you actually use them.

September 2019 Update: New Sign-Up Offers

- Chase IHG Premier: 125,000 IHG points + $50 statement credit after spending $3,000 in three months. The bonus and credit are worth $675 at current point valuations, or $586 net of the $89 annual fee that isn’t waived. This is the highest ever sign-up bonus for this card.

- American Express Hilton Honors: 100,000 Hilton points after spending $1,000 in three months. Use incognito mode or private browsing to see the offer. The bonus is worth $600 and the card doesn’t have an annual fee. It’s best to apply for Amex cards when sign-up offers are at all-time highs (like this one) since Amex limits people to one sign-up offer per card per lifetime.

- Chase Freedom and Chase Freedom Unlimited now offer 20,000 Ultimate Rewards points after spending $500 in three months. The bonuses are worth $400 if used for UR redemptions and not cashback. Neither card has an annual fee.

- Apple Card: This is a new card with no sign-up bonus. The card earns 3% cash back on Apple purchases, 3% on Uber and UberEats via ApplePay, 2% elsewhere via ApplyPay, and 1% on everything else. You can find better returns on everyday spend with cards like the Chase Freedom Unlimited or American Express Everyday Preferred.

- Banco Popular Avianca Vuela: 40,000 Avianca LifeMiles after first purchase and 20,000 after spending $1,000 in three months. Use code SB4060. 60,000 LifeMiles are worth $1,020 or $871 net of the $149 annual fee. Avianca is a member of the Star Alliance so you can use LifeMiles on a variety of carriers. The LifeMiles program is unique because it doesn’t impose any fuel surcharges.

September 2019 Update: News and Resources

- United Airlines miles no longer expire. They previously expired after 18 months of inactivity. Most programs like American’s AAdvantage have expiration dates but it’s easy to generate activity without actually redeeming miles for a flight.

- Chase Ultimate Rewards now directly transfer to Emirates Skywards. It’s good to have another transfer partner but there are few high value Skywards redemptions. The Emirates program involves steep fuel surcharges ($500+) for long-haul flights.

- Norwegian Airlines is negotiating a bond extension. Norwegian is the only low-cost transatlantic carrier after WOW airlines went bankrupt in March. It’s pretty common to be able to fly Norwegian round-trip from the east coast to Europe for <$250. Norwegian has $380 million in principal repayments over the next few months and are trying to extend it into 2021 and 2022.

- Two useful guides were published last month: the best cards for grocery store spend and a compilation of point transfer times.

The Best Sign-Up Bonuses

The spreadsheet calculates the after-fee sign-up bonus value for 86 cards as of September 2019 and includes the following for each card:

- Current sign-up bonus

- Point program’s approximate value (via The Points Guy)

- Annual fee and whether the first is waived

- Minimum spending requirement for the sign-up bonus

Here’s a link to a full-screen version of the spreadsheet in Google Docs. The spreadsheet has tabs at the bottom for each type of card.

There’s a wide range in sign-up bonus values. For example, you probably shouldn’t apply to US Bank or Wells Fargo cards since their bonuses are worth so little. In contrast, the Chase Sapphire Preferred and Citi Premier cards make it fairly easy to get $1,000 of free travel.

Other Important Things You Should Know

- You need to have an application strategy: Banks have gotten stricter with card applications. Chase has a 5/24 rule, meaning you can’t get approved for most Chase cards if you’ve opened more than 5 cards within the past 24 months. Before signing up for any card, step back and ask 1) what type of travel do you want to book and 2) what card and loyalty programs provide the highest redemption value for that type of travel.

- Point devaluations: Airlines and hotels change the redemption value of their award charts. For example, American Airlines might require more miles for the same flight or Hyatt might shift a hotel from a category 2 to a category 3. Devaluations are slow, typically occurring once a year, but they are persistent. The true value of a large points balance will slowly erode over time.

- Avoiding annual fees: Most cards can be downgraded to a free version before or immediately after an annual fee is due. For example, I downgraded my Chase Sapphire Preferred to a no-fee Chase Freedom after earning the sign-up bonus.

- Credit score impact: You should only apply to a rewards credit card if you have a stable job and existing credit history. Those without credit are better suited for a secured credit card. Opening a new card does lower your credit score marginally for a brief period, but this disappears as the account ages. Here’s a good article on how credit cards impact your credit score.

- Business cards: The spreadsheet I made is for personal cards. There are also ~30 business cards with sign-up bonuses.

- Incognito mode: Some card offers change based on your location or browser history. Use incognito mode (Chome) or private browsing (Firefox/Safari) to ensure you see the highest publicly available offer.

Useful Resources

- Award Hacker: Shows you how many points it takes for a given flight. Much quicker than looking up redemption tables

- Award Mapper: Shows hotel categories and their required number of points for a given destination

- Credit Card Tune Up: Based on your spending inputs it will show the card with the highest value for your everyday spending

- Transfer Partner Calculator: Shows the conversion rate of transferring points between partners

- Simple Dollar Cashback Card Guide: Shows the best cashback card for your spending habits

- List of all airline alliance members

The Cards I Use

I don’t use credit cards for discretionary personal spending. There was a time when I had five cards in my wallet and used them based on which would maximize points for a given purchase.

Then I stumbled across research on how the average person spends more with a card relative to cash. Basically, using a card makes money feel less “real” so you tend to be less rational with it. In January, I switched to using cash for all in-person spending and put card-only payments on my debit card. My discretionary spending has been 10% lower this year compared to 2018. No credit card is going to give you a 10% return on everyday spending. The highest “return” on everyday spending might, ironically, be through avoiding cards and using cash.

There is still significant value in sign-up bonuses and later this year I’ll apply for a few new cards.

Summary

- Use credit card points for booking travel, not statement credits

- Flexible point programs tend to be more valuable than program points (since you have more redemption options)

- Flexible point programs are not restricted to immediate transfer partners and can be used with alliance members

- There can be a huge difference in redemption values between alliance members, so search before you book

- The sign-up bonus is the most valuable part of a credit card. The spreadsheet converts bonuses into expected redemption values

- Before you apply for a card, think about the travel you want to book and which cards have the highest redemption value

- Avoid annual fees by calling your credit card company and asking to downgrade to a no-fee version

Feel free to send me a message if you have questions about the spreadsheet, the best card for you, or the best redemption for a given trip.