Measuring the All-In Fee of Top Investment Advisors

An analysis of how much the average advisor truly costs and what it means for future returns.

Fees really matter. The goal of this post is to show the true cost of professional management for a $1 million portfolio.

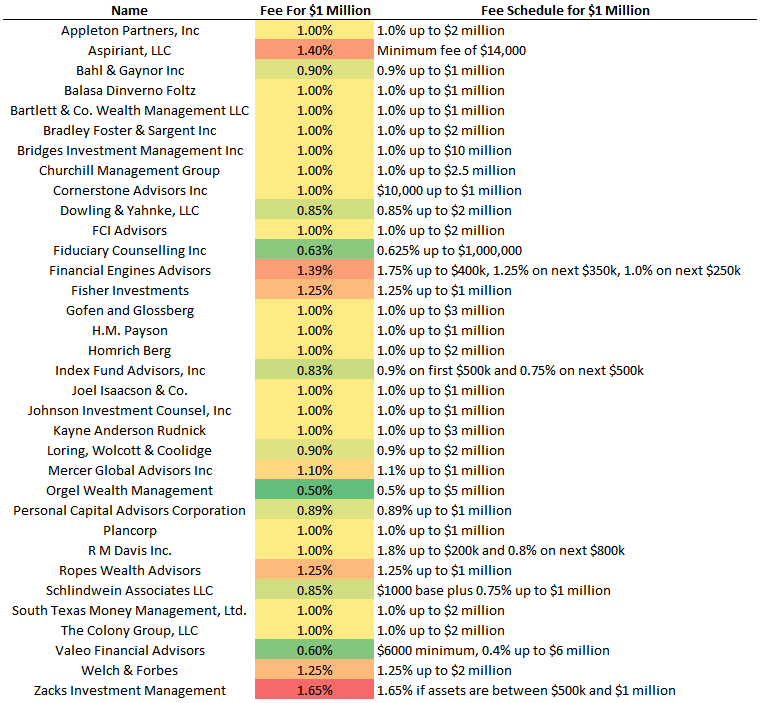

I went through ADV disclosures for each of the top 100 RIA firms in the InvestmentNews database. I then excluded family offices with high minimums and firms with variable pricing not clearly broken out into tiers. Some of the firms include financial planning in their fee and most firms have discretion so clients might pay less than the public fee.

Here’s the data:

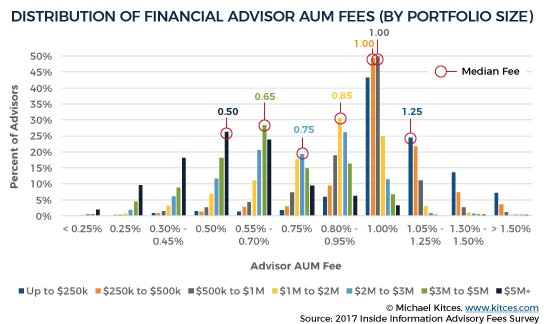

The median annual fee to manage $1 million is 1.0% per year. This is a bit above the 0.85% that Michael Kitces found:

Implementation Cost

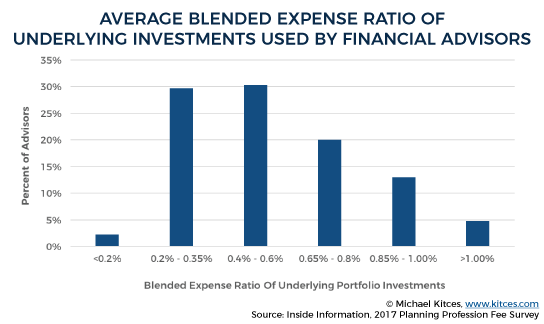

An advisor’s true cost is more than just their management fee. You also need to know how much it costs to implement their strategy. This implementation cost is a combination of fund expense ratios, transaction costs, and taxes. For simplicity’s sake I’ll ignore transaction costs and taxes, since they are highly variable and even non-existent for passive buy and hold managers.

We do have concrete data on expense ratios. The blended average expense ratio of funds that advisors use is 0.50%.

When added to the management fee of 1.0%, the average advisor has an all-in cost of 1.5% per year.

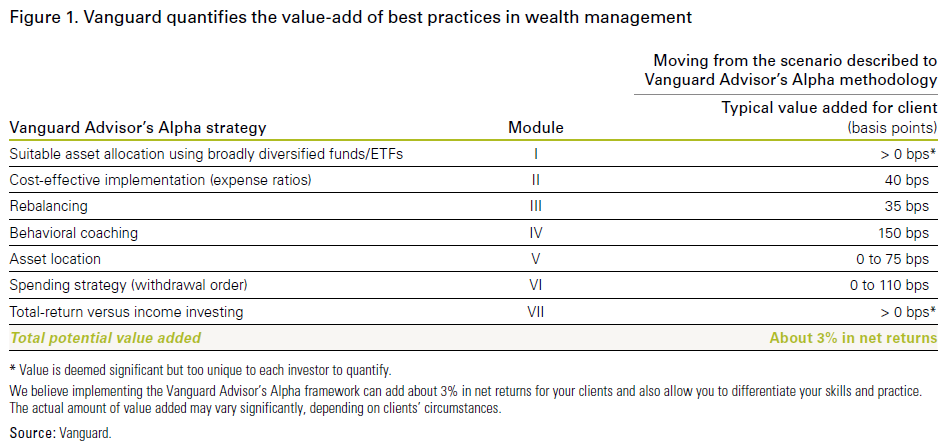

A common rebuttal is that advisors are worth their fee since they add “advisor alpha.” I agree that competent advisors who provide behavioral coaching, low-cost fund selection, and increased tax-efficiency will provide higher returns than what a typical investor could achieve on their own. I just don’t think this is worth the 3% in value that’s typically quoted.

{kind=link}

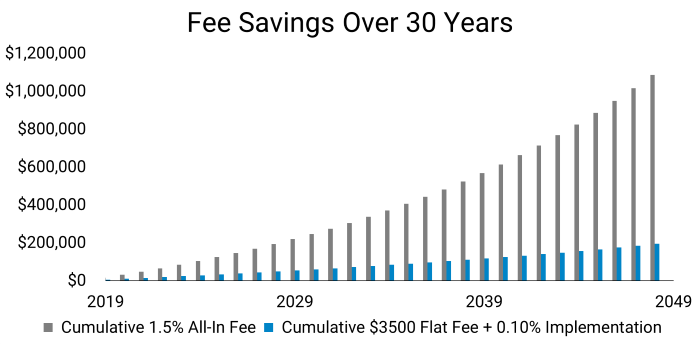

Fee Impact on Financial Goals

Percentage fees are an abstract concept for the average investor and it’s important to connect fees to real-world goals.

Imagine two hypothetical investors with $1,000,000:

- Both earn 7% gross per year.

- One investor pays an advisor an all-in 1.5% per year for management and implementation.

- The other investor pays an advisor a flat annual $3,500 management fee and 0.1% per year in implementation costs.

The second investor saved $892,000 over 30 years.

That could mean retiring a few years earlier or covering college for all of your grandchildren.

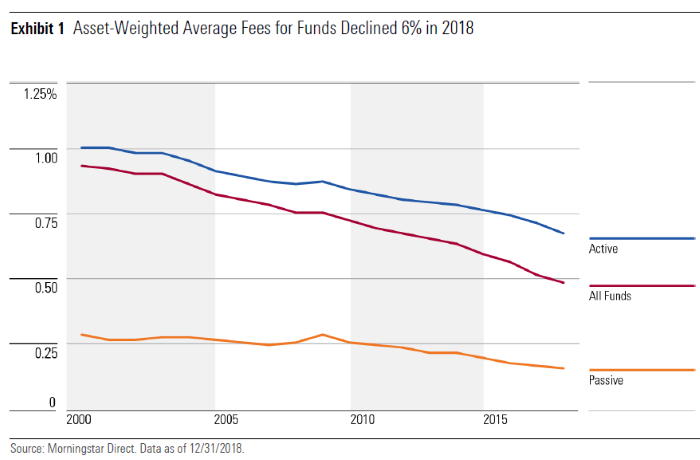

Financial product fees have been cut in half since 2000:

I expect the same thing will happen to the cost of financial advice. I started my RIA charging the typical 1.0% and recently switched to a flat fee to get ahead of what I think is an inevitable shift toward more competitively priced financial advice.

Fee Impact on Returns

Fees have been small relative to returns of the recent bull market. Going forward, they’ll likely consume a bigger slice of investor returns.

To estimate stock returns I took an average from Morningstar’s 2019 return estimates. Companies like Vanguard and Blackrock expect U.S. stocks to return 4% nominal over the next decade. They expect a higher 6% from international stocks. So 5% is a baseline estimate for what a globally diversified investor can realistically expect to earn. Bonds are easier to forecast since future returns are highly correlated to starting yields. The 10-year Treasury’s current yield of 1.6% is a good baseline for bonds.

An example 60/40 portfolio can be expected to earn 3% from the stock allocation (5% * 0.6) and 0.64% (1.6% * 0.4) from the bond allocation, or 3.64% for the total portfolio. After paying the average management and implementation fee of 1.5% you’re left with 2.14%. The 1.5% fee represents 40% of gross returns. You’re left with 0.14% per year if annual inflation averages 2%.

I genuinely hope stocks and bonds deliver higher returns than this. But hope isn’t a strategy and high fees raise the probability that a portfolio’s inflation-adjusted value will tread water over the next decade.

Summary

- The average advisor fee to manage a $1 million portfolio is 1.0% per year.

- The true cost of an advisor also factors in their implementation cost. This is typically around 0.5%.

- All-in fees north of 1.5% will likely be a substantial drag on portfolio performance over the next decade.