The Largest Arbitrage Ever Documented – TIPS in 2008

A story behind the dislocation of TIPS and Treasuries.

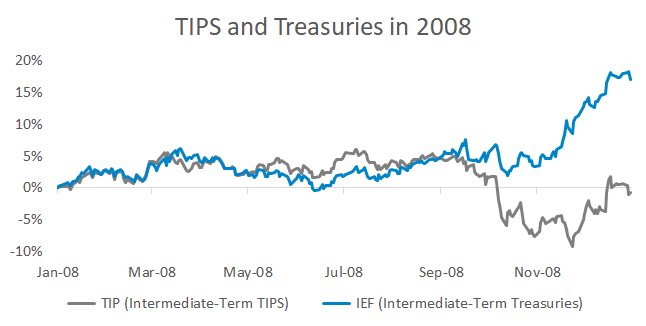

One issue with TIPS is their performance in 2008:

Some investors say “TIPS didn’t protect you in 2008, so I’m not using TIPS because that’s when bonds should work.”

The Lehman Brothers bankruptcy is at the heart of why the TIPS market acted so strangely. In 2009 the United States Government Accountability Office wrote:

“Lehman Brothers owned TIPS as part of repo trades or posted TIPS as counterparty collateral. Because of Lehman’s bankruptcy, the court and its counterparty needed to sell these TIPS, which created a flood of TIPS on the market.”

Lehman’s counterparties and the bankruptcy court were forced sellers. A relative value fixed income fund named The Barnegat Fund was on the other side of the trade.

Barnegat noted the triple whammy facing TIPS in 2008:

- Forced unwind of Lehman collateral

- Real return funds took a bath on commodities and were also forced to sell TIPS

- Nobody was interested in allocating to relative value funds like Barnegat – letting the arbitrage persist for longer

Barnegat bought TIPS, shorted Treasuries, and hedged out the inflation risk with inflation swaps. Without the swaps the trade would be a direct bet on inflation.

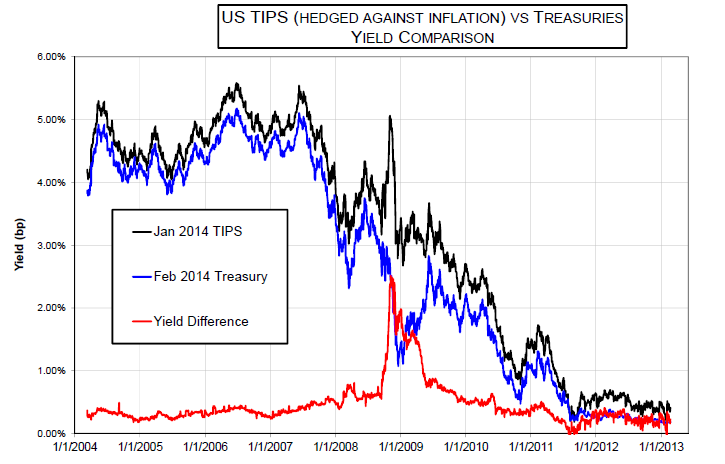

There wouldn’t be a huge arbitrage opportunity if TIPS were accurately reflecting inflation expectations. But the inflation swaps market wasn’t affected by the forced TIPS selling and priced in a less deflationary future than TIPS.

At its peak, the trade netted 2.5% on unleveraged capital with zero credit risk, zero rate risk, and zero inflation risk. Barnegat returned +132% in 2009 and researchers nicknamed the trade “the largest arbitrage ever documented in the literature.”

Geek Note: A number of funds had this trade on but some were unable to hold it through the crisis. A letter from Barnegat explains two of the unique ISDA clauses that helped them hold the trade to maturity.

Here’s a video of Barnegat’s founder talking about the trade:

While TIPS have been more positively correlated to stocks than regular Treasuries, their performance in 2008 was more of a one-off event than a blueprint for how they’ll perform in the next downturn.

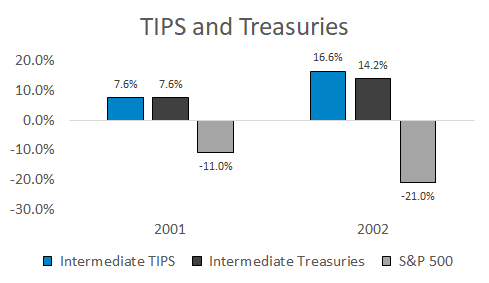

For example, TIPS and Treasuries closely tracked each other during the early 2000s recession:

This is the third in a 5-part series on TIPS. Here are links to the other posts: