The Origin of TIPS, How They Work, and an All Weather Mistake

A historical look at inflation-indexed bonds, how they perform differently than regular bonds, and data on how few investors own TIPS.

In 1963 James Tobin said:

“Markets do not provide, at any price, a riskless way of accumulating purchasing power for the future.”

Fortunately for modern investors, we can buy Treasury inflation-protected securities. I rarely see TIPS in prospective client portfolios and the next few posts explain why I use them.

Inflation-indexed bonds fill an important gap in the fixed income market. Regular Treasury bonds are riskier than they seem – long-term Treasuries fell 60% in inflation-adjusted terms between 1940 and 1981. Shortening duration is not a solution since real rates for short-term Treasuries have been as low as -9%. TIPS solve these issues by offering a safe bond investment not vulnerable to inflation.

The next five posts will cover all aspects of the TIPS market. To kick off the series, here’s some historical context on how TIPS came to be:

History of Inflation-Indexed Bonds

- May 1780: The first inflation-indexed bonds were issued by the Commonwealth of Massachusetts to soldiers during the Revolutionary War. Wartime inflation meant soldier pay rapidly decreased in value between when it was promised and when it was paid. 1780 was a low point in the war and inflation-indexed bonds were viewed as a way to increase soldier morale.

- March 1981: The UK was the first major country to issue inflation-indexed bonds – nicknamed “linkers” since they are linked to inflation. Annual British inflation peaked at 27% in 1975, much higher than in the US. The 1981 bond was restricted to institutional investors. Pension funds have a natural need for inflation-indexed bonds since future liabilities are typically tied to inflation.

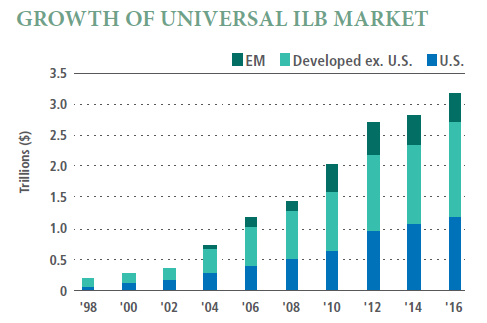

- January 1997: The US first issued TIPS in 1997. The first few years were defined by slow acceptance and high real yields that look like a bargain in retrospect. The US is now the world’s largest single issuer of inflation-linked bonds, closely followed by the UK and Brazil.

How TIPS Work

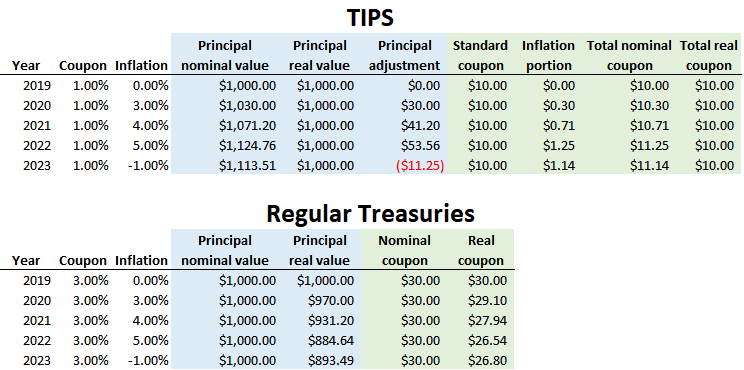

TIPS are different than regular Treasuries in two ways:

- The principal value of a TIPS bond is adjusted based on inflation

- Coupon payments are based on this adjusted principal value

The easiest way to show this is with an example:

Unlike a regular Treasury where the inflation-adjusted principal erodes over time, the real value of a TIPS bond holds steady. The coupon also increases with inflation since it’s based on a higher principal value. This is why a TIPS yield is called a real yield.

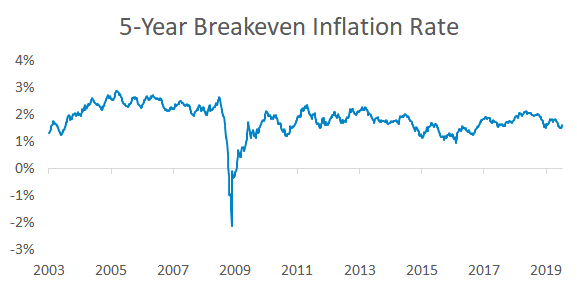

The breakeven inflation rate is the difference between a TIPS yield and a Treasury yield of the same maturity. It’s the inflation rate where owning TIPS and owning Treasuries would result in the same inflation-adjusted cash flows. There’s an interesting story behind the big drop in breakeven rates in 2008 – I’ll write about that on Friday.

TIPS offer unlimited potential outperformance over Treasuries in inflationary environments, while regular Treasuries only offer limited potential outperformance over TIPS in deflationary environments. The limited Treasury outperformance during deflation is because TIPS have a deflation floor. At maturity, a TIPS investor receives the higher of the adjusted principal value or the original principal value.

The deflation floor is most relevant for newly issued TIPS with principal values close to par. The most important thing to remember about TIPS is that they protect against unexpected inflation. Expected inflation is built in to the yield of a regular Treasury bond.

TIPS Market Share and an All Weather Mistake

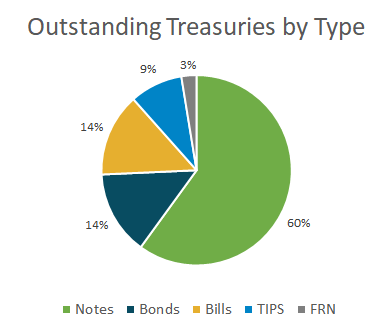

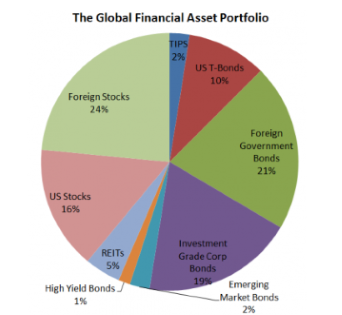

TIPS make up 9% of outstanding Treasury debt and only 2% of global financial assets.

Bridgewater was instrumental in developing the TIPS market.

The All Weather strategy allocates an equal amount of risk between assets that perform well in different economic environments. Inflation-linked bonds are one of the few assets that have historically worked in two environments: falling growth and rising inflation.

All Weather strategies gained mainstream attention in 2014 when Tony Robbins wrote about the approach in Money: Master the Game. A Google search for “all weather ETF strategy” shows articles suggesting this portfolio:

- 40% long-term regular Treasuries

- 30% stocks

- 15% intermediate-term regular Treasuries

- 7.5% commodities

- 7.5% gold

This is not an all weather portfolio. The 55% in regular bond exposure will significantly underperform if inflation accelerates. Portfolios structured for all potential economic environments need TIPS due to their unique inflation hedging characteristics.

Summary

- Inflation-indexed bonds were first used to protect the purchasing power of soldiers in the Revolutionary War.

- Both the principal value and coupon of a TIPS bond are adjusted based on inflation.

- TIPS are a small segment of the bond universe and few investors own them.

This is the first in a 5-part series on TIPS. Here are links to the other posts: